Introduction

Organisations like Johnson and Johnson, P and G, Shell create shareholder value by having an inspiring vision, clear strategies,, rigorous segment and brand prioritisation, consistent innovation, superior value propositions, high employee morale, tight cost control and concern for all stakeholders. Our best scholars have argued this case for decades and the proof that ignoring stakeholders other than shareholders does not pay off in the long run is beyond doubt.

Short termism has without doubt been the principal enemy of marketing. Any fool can maximise profit by cost cutting, downsizing and the like, especially in growth markets, but without getting the stakeholder balance right, disaster eventually ensues. ICI was a classic example of being benign to stakeholders, but who systematically destroyed shareholder value and in the process destroyed whole communities.

This article argues that without creating shareholder value added (SV), even if they pay attention to all other stakeholders, organisations have no future.

It then sets out a methodology for risk assessment for the C-Suite which will ascertain whether the marketing strategy creates or destroys SV.

The Central Role of Risk Assessment in Value Creation

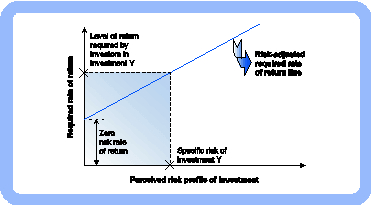

Let’s first look at the concept of risk. For most companies, the current share price already reflects some expected future growth in profits. Thus, these current investors and, even more particularly, potential future shareholders, are trying to assess whether the proposed business strategies of the company will produce sufficient growth in sales revenues and profits, both to support the current share price and existing dividend payments and to drive the capital growth that they want to see in the future. At the same time they also need a method of assessing the risks associated with these proposed strategies as, obviously, these will have a direct link to their required rate of return. This is where marketing can play play a role. As Figure 1 shows, the perceived risk profile of the investment drives the level of return required by investors in each particular investment.

Figure 1 Risk-adjusted required rate of return

Logically, therefore, a normal, rational, risk-averse investor requires an increase in expected future return from any more risky investment in order to compensate for any potential volatility.

No amount of discussions will alter this inarguable fact of life. It was ever thus and certainly long before Rappaport proposed EVA (the antecedent of SV).

In most government-backed debt investments investors know in advance exactly what their return will be (i.e. the interest rate payable is stated on the debt offering). However this is clearly not the case with most equity risk perceptions and hence required rates of return. Further, if the historical track record of a company’s shares shows significant volatility in share prices and even dividend payments, investors will require much higher returns from the company as they extrapolate from this past performance to the future likely performance of the company’s shares. Thus, life is much more challenging for a highly volatile company, caused by shareholders’ natural dislike for risk.

The new opportunity for CMOs from SV

In the best companies, senior managers carry out proper due diligence on declared future business strategies, taking into account the associated risks, the time value of money and the cost of capital.

Optimal business strategies seek to increase returns whilst reducing associated risk levels and it is these that will create SV. Remember, investors are interested in SUSTAINABLE shareholder value, as it is this which impacts the capital value of shares, not results in a single year manipulated by short termism on the part of managers.

Whether we like it or not, SV will persist as the most logical method of measuring corporate performance, for unless it is created, all stakeholders will suffer. This provides an unprecedented opportunity for CMOs to show the true worth of their work, especially as today intangible assets, (which of course include relationships with customers) now account for about 65% of all corporate value in the UK.

I set out below a very clear methodology for calculating whether marketing strategies create or destroy shareholder value. It is this level of sophistication that will get the undivided attention of the boardroom.

Valuing Market Strategies

Background/facts

- Risk and return are positively correlated, ie as risk increases, investors require a higher return.

- Risk is measured by the volatility in returns ie high risk is the likelihood of either making a very good return or losing all your money. This can be described as the quality of returns.

- All assets are defined as having future-value to the organisation. Hence assets to be valued include not only tangible assets like plant and machinery, but intangible assets, such as customer relationships.

- The present value of future cash flows is the most acceptable method to value assets.

- The present value is increased by:

- Increasing the future cash flows

- Making the future cash flows ‘happen’ earlier

- Reducing the risk in these cash flows, ie improving the certainty of these cash flows, and, hence, reducing the required rate of return.

Suggested Approach

- Identify your key products for markets.

- Based on your current experience and planning horizon that you are confident with, make a projection of future net free cash in-flows from your markets. It is normal to select a period such as 3 or 5 years.

- These calculations will consist of three parts:

- Revenue forecasts for each year

- Cost forecasts for each year

- Net free cash flow for each product for market for each year.

- Identify the key factors that are likely to either increase or decrease these future cash flows.

- These factors are likely to be assessed according to the following factors:

- The riskiness of the product/market.

- The riskiness of the marketing strategies to achieve the revenue and market share.

- The riskiness of the forecast profitability (e.g. the cost forecast accuracy).

(Please note that a detailed methodology for doing these calculations is spelled out in McDonald M et al “Marketing and Finance “ Wiley 2013

- Now recalculate the revenues, costs and net free cash flows for each year, having adjusted the figures using the risks (probabilities) from the above.

- Ask your accountant to provide you with the overall SBU cost of capital and the capital used in the SBU. This will not consist only of tangible assets. Thus, £1,000.000 capital at a required shareholder rate of return of 10% would give £100,000 as the minimum return necessary.

- Deduct the proportional cost of capital from the free cash flow for each segment for each year.

- An aggregate positive net present value indicates that you are creating shareholder value – i.e achieving overall returns greater than the weighted average cost of capital, having taken into account the risk associated with future cash flows.

Three actions for CMOs

There are only three things a CMO can do to influence SV. The first is to invest in markets and customers that earn more than the cost of capital. The second is to reduce expenditure on customers and markets that earn less than the cost of capital. The third is to reduce the risk inherent in their strategies.

Measurable benefits to the business

With legislation around the world placing more and more emphasis on control procedures and corporate governance, and with the increasing potential penalties on individual directors, the need for an objective, recognised and well-structured review and approval process should be obvious.

Professor Malcolm McDonald